Related Content

Financial services consulting

Mazars’ regional financial services consulting team aims to assist clients in exploiting key growth opportunities to deliver superior economics.

Here we examine the problem from the perspective of the deposit taking institution. We will not attempt to predict the future direction of interest-rates. Instead, we will focus on concrete actions that can be taken to address the current challenges which may, or may not, persist for some time. We will address both cost and revenue drivers and illustrate this with the help of a recent example of how a bank in South-East Asia took on the challenge.

The key challenge of a low interest rate environment is that interest costs (paid on deposits) do not reduce at the same rate as interest rate revenues (received from loans). Typically, interest costs have a hard floor; once you’ve already moved to zero or near-zero interest rates on parts of the portfolio, it’s hard to go further. However, there are other issues that can be addressed, as even in such an environment the cost of gathering deposits is far from negligible. Here we will take a product perspective and focus on both the direct interest costs and also the other product-related costs that go into deposit gathering. We will not touch the marketing, distribution and servicing costs that banks can and should also address to reduce the overall cost to serve.

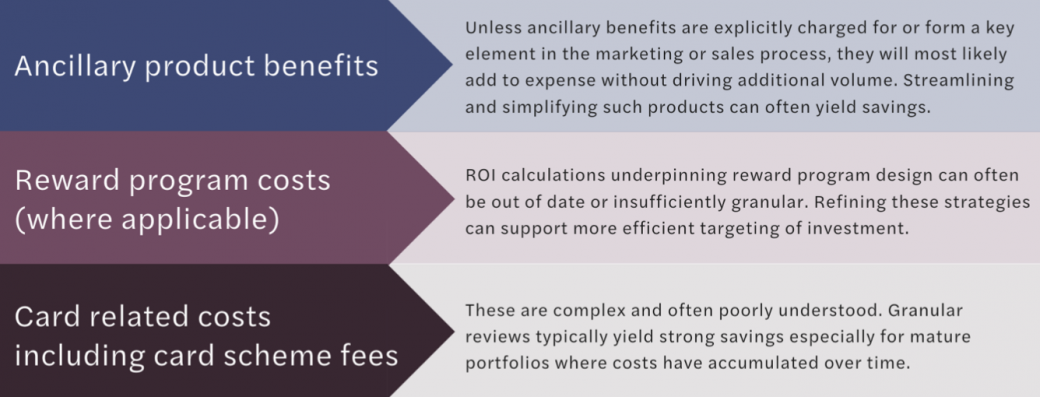

It is common to find that even when interest rates are near-zero on parts of the portfolio, other parts will have higher pricing, either by design (e.g. fixed-term deposits) or by neglect (e.g. legacy issues or niche products). By undertaking a granular review of the full portfolio, material savings in interest expense can be made.

Indeed, in a recent review for a bank in SE Asia Mazars consultants found that pricing for a specialist product had not been adjusted in line with the rest of the portfolio, and also that anomalies in the interest calculation methodology were causing expenses to be higher than they should have been. Correcting these issues through simple adjustments would reduce interest expense by 5.5% and increase net interest income by 2%. Such results are broadly in line with what we have observed across multiple other institutions.

Beyond interest, there are multiple other product-related costs that typically apply to deposit gathering. In a low interest rate environment the importance of each of these is magnified, so close attention is advised. Savings can often be found in the following areas:

Cost reduction alone is unlikely to be sufficient to make up the shortfall caused by margin compression. Attention must also be turned to growing top-line revenues in the form of fee-based income, unaffected by prevailing interest rates. Here we will examine 3 strategies that can be usefully deployed:

Before looking to introduce new fees, banks must first make sure to fully collect those already in place. In our experience, too often this is not being done as well as it should. System glitches, manual waivers, or more often a lack of proper enforcement, can lead to fees being under-collected. Common problem areas include:

In a recent engagement Mazars consultants found that over 5% of fee income was not being collected due to inadequate enforcement. Such results are quite typical for banks that have yet to fully address such issues. The good news is that once properly diagnosed, corrective action is usually straightforward.

In a composite pricing model the bank looks at the total revenues and costs in aggregate at a product or customer level. It does not matter if revenues cover costs at a lower level so long as they are sufficient in aggregate. In many markets deposit related costs such as over-the-counter deposits and withdrawals and not covered by direct charges, but instead cross-subsidised by the interest spread on deposits. As interest margins get compressed in a low-rate environment, more emphasis needs to be placed on fee-based income lines to make up the difference.

Similarly, in the commercial and corporate banking sectors where pricing agreements are often individually negotiated it is common to find instances where customers have specifically agreed to maintain higher deposit balances in return for the waiving of service fees. Those agreements are likely to come under strain as the value of these deposits decreases. Increasing deposit requirements further may not be practical, and instead these agreements may need to be unwound and service fees reinstated.

Reducing leakage and rebalancing income streams are valuable and necessary steps, but on their own are insufficient to drive true growth which must be driven by innovation and improvement. Everyday improvements to the core offer will deliver competitive advantage, but extension into new categories through added-value packages of services can drive incremental fee income. In many markets we observe that banks are on the defensive, concerned about new entrants competing to take slices of their profitable businesses. In our view they should take these threats seriously, but at the same time look to take advantage of their scale, customer base and trust to compete in new areas themselves either independently or as part of a wider eco-system.

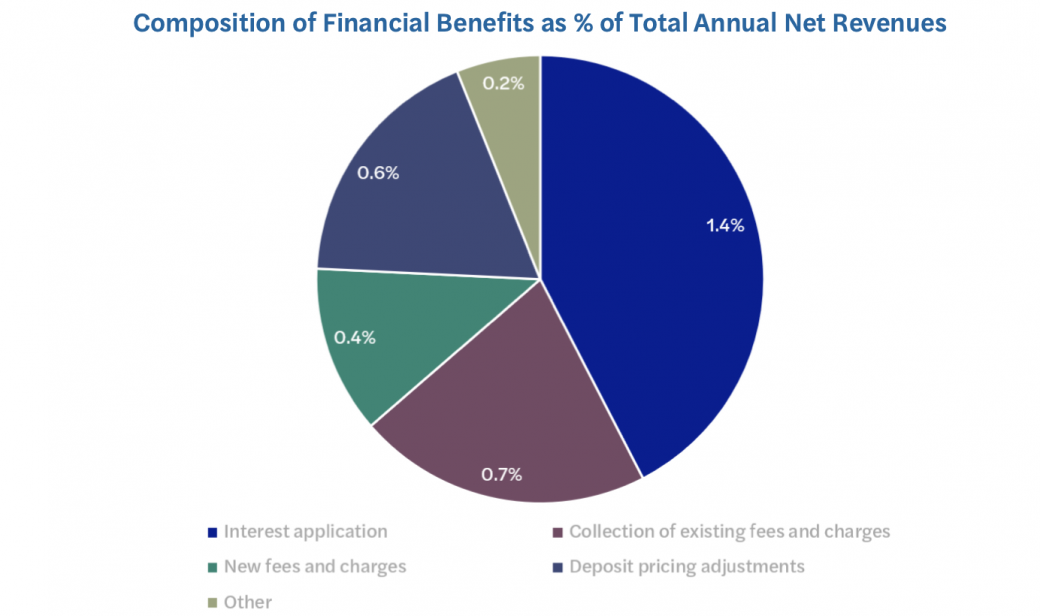

The chart below, taken from a recent engagement with a bank in South-East Asia, illustrates how such strategies can collectively improve the financial performance of a deposit-taking business. In this case the financial benefits equated to 3.4% of net revenues and approximately 16% of estimated net profit. Similar results have also been achieved by other banks in multiple markets.

Composition of Financial Benefits as % of Total Annual Net Revenues

Summary

In summary, the challenges to physical distribution that have been raised by the global pandemic have led banks to double down on digital transformation, sometimes at the cost of other commercial activities. This is understandable, but it need not be an either/or decision. The financial challenges of a low interest rate environment are significant and warrant attention. Deposit taking institutions need to make adjustments to their revenue models and continue to carefully manage costs in order to thrive. In our experience there is much that can be done at the product level to improve efficiency in the near term and even more that can be done to build additional sources of revenue through further innovation.

Mazars’ regional financial services consulting team aims to assist clients in exploiting key growth opportunities to deliver superior economics.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.